-

General

-

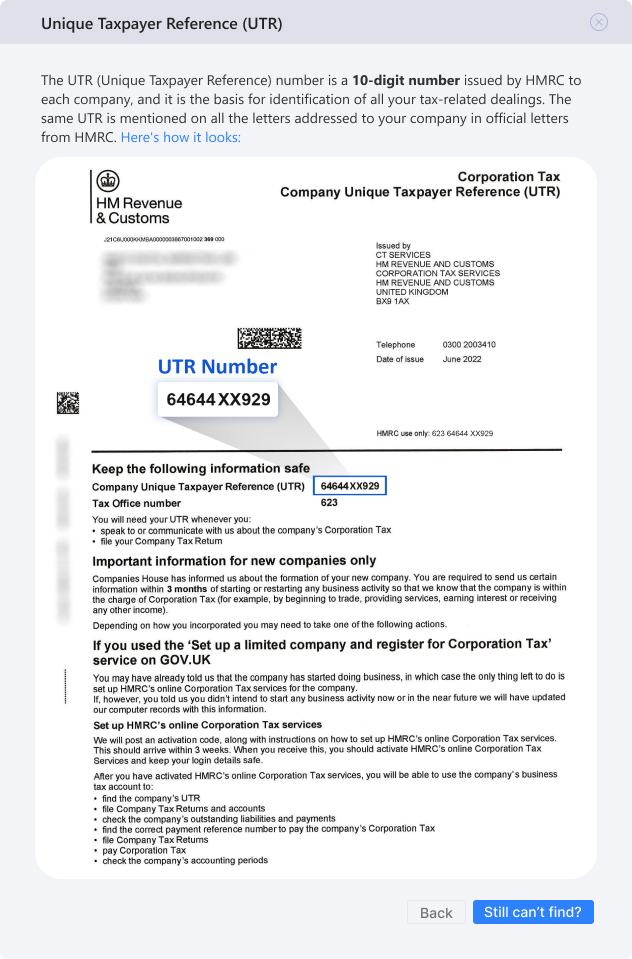

What is UTR (Unique Taxpayer Reference)?

A UTR (Unique Taxpayer Reference) number is a 10 digit code that's unique to either you or your company. It facilitates HMRC to process tax returns in an efficient, effective and accurate manner. It helps to identify the person (i.e. whether it's a company, partnership etc.) so that their records can be managed accordingly. It also helps in ensuring that everyone pays what they owe or receive amounts they might be entitled to correctly.

-

Why does the HMRC need my UTR (Unique Taxpayer Reference)?

UTR number is a 10 digit unique code issued by HMRC to all the entities whether individuals, limited companies, LLPs etc. HMRC needs the UTR number to identify the person or sole proprietor for return filing and tax payment purposes.

-

How do I know my tax-free income through tax codes?

- A tax code is an alphanumeric code used to work out how much income tax needs to be collected from your income.

- These codes generally start with a number and end with an alphabet, for e.g., 1257L. The number in a tax code denotes the amount of tax-free income you get in that particular year.

- The letter in the tax code refers to your personal circumstances which may affect your Personal Allowance.

-

What are different types of errors that can occur while finalising a Trial balance?

Various types of trial balance errors are as follows:

The error of Principle:

When a transaction is recorded in a manner that any of the generally accepted accounting principles is violated then it is called error of principle. There isn't any effect on trial balance in such cases as the amount is correctly posted on debit-credit sides but the accounts are incorrect. Such errors can cause the financial statements to depict a misleading picture of the affairs of the business.Omission Error:

There can be two kinds of error of omission- complete and partial. Complete omission means that a transaction has been missed to be recorded in the journal. There isn't any effect on trial balance in such cases. Partial omission means that a transaction has been recorded in the journal but omitted to be posted into the ledger accounts. Such kinds of omissions hamper the agreement of trial balance.Commission error:

Such errors generally relate to arithmetic accuracy. These include recording wrong amount in subsidiary books, wrong totalling of subsidiary books, posting incorrect amount in ledger accounts, posting at the wrong side of ledger accounts, incorrect totalling of ledger balances etc. These may or may not cause trial balance totally.Compensating errors:

If two or more errors are committed in a manner that the effect of one error is compensated by the effect of other error, then such errors are called compensating errors. These errors leave agreement of trial balance unaffected. -

What are the effects of over-reporting and under-reporting in accounts submitted to authorities?

Over reporting- Once you file your accounts to Companies House and HMRC, they come into the public domain. Over reporting in the accounts can cause your competitors to know your business strategy and they could easily take undue advantage of this.

Underreporting- Underreporting to Companies House and HMRC can cause them to take action against you. You might end up paying heavy penalties.

-

How will early filing of accounts benefit me? Or why should I file my accounts early?

Filing your accounts early before the due date has its own benefits.

Some of them are:

- No worrying about deadlines.

- No fear of paying penalties for late filing.

- Extra time to make any amendments.

- Cash Flow Management - Nothing is ever guaranteed in business or life, apart from death and taxes. You will have to pay taxes on your profits that are a certainty. It’s advantageous to have all of the information as early as possible so that you can budget appropriately and ensure that you have the necessary funds ready to pay your tax bill when the time comes.

- Peace of mind - Businesses can be stressful at times and you rarely know what is coming up in the future. This is an opportunity to gain more clarity over the financial future of your business and at least understand and factor future outgoing payments into your plans.

-

What is the difference between the accrual basis of accounting and cash basis of accounting?

Cash basis of accounting deals with recognising revenues- when cash is actually received and expenses- when cash is actually paid. In this method, there is no requirement of keeping a track of receivables and payables. The business income isn't taxed until it's received in cash or in a bank account. It is easier to maintain. The disadvantage of this method is that it ends up giving a biased view of the business as an expense and its related revenue might get reported in different periods.

Accrual basis of accounting deals with recognising revenues when they are earned and expenses when they are incurred, irrespective of the date of actual payment. irrespective of the fact that whether the money has been received/paid. This method works on matching principle which means the expense is reported in the period when related revenues are earned. This method gives a true and significantly better view as compared to the cash basis of accounting.

-

What is HMRC gateway account?

The HMRC Gateway account is an account created to use online services provided by HMRC. To sign in the HMRC gateway one needs 12 digit Government Gateway user ID and password.

-

Where can I find my UTR (Unique Taxpayer Reference) number?

UTR (Unique Taxpayer Reference) is automatically sent when you register for self-assessment or set up a limited company. It can be found on your:

- Previous returns

- Payment reminders or notices to file returns received from HMRC at your registered office address.

- You can call the self-assessment helpline on 0300 200 3310 to request your UTR if you cannot find any documents from HMRC.

- For a limited company, we can request your Corporation Tax UTR online. HMRC will send it to your business address that is registered with the Companies House.

-

What is a benefit in kind?

Benefit in kind refers to:

- Asset or service provided by the employer to employee,

- that is used by employee personally but is paid for by a company

- and isn't “wholly, exclusively and necessary” for business purpose.

Benefits in kind need to be reported in the form P11D. They are treated as cash equivalents and so are taxed as a part of your (employee’s) salary.

-

Does the employer need to report the HMRC for a trivial benefit?

If the employer provides trivial benefit as a part of the salary sacrifice arrangement, then they won’t be exempt. The employer will have to report it to the HMRC in form P11D.

- The salary is given up or

- How much you paid for the trivial benefits, whichever is higher.

However, the director of a ‘close company’ cannot receive trivial benefits worth more than £300 in a tax year.

-

What is the minimum wage?

The government has prescribed minimum wage rates i.e., the minimum amount per hour that any worker should be paid. Workers above the age of 25 are entitled to National Living Wage which is highest of the National Minimum Wage. The wages amount determined using these minimum wage rates is called minimum wage.

-

What are benchmark scale rates?

Benchmark Scale rate payments are basically the maximum tax and NICs free amount that can be paid or reimbursed by the employers to their employees in respect of common business expenses incurred by the employee, without requiring any approval from HMRC.

-

What is Auto-enrolment of pensions?

As per the Pension regulators guidelines, the employer has to auto-enrol all its employees under a workplace pension scheme and also contribute a prescribed percentage of the salary as an employer's contribution. Any employers in the UK fulfilling the below conditions are bound by this legislation:

- if they employ at least 1 person

- such person/persons earn more than £10,000 a year

- such person/persons are aged between 22 and State Pension Age

-

How do I know which period is considered as the financial year?

The period falling between two accounting reference dates is considered as the financial year. It is also known as an accounting period.

-

How do I know which period is considered as an accounting year?

The period falling between two accounting reference dates is considered as an accounting year. It is also known as a financial year.

-

Can I claim for deductions as Capital allowance?

Capital allowance refers to deductions allowed from the profits with respect to certain assets purchased which have a useful life of more than one tax period. Click here to read about capital allowances in detail.

-

How do I know which day is considered as the accounting reference date?

When your company is formed, the first accounting reference date will be a year later, on the last day of the month in which your company was incorporated. The accounting reference date will then be on this date every year until we change the accounting period.

-

What do you mean by Business mileage claim/allowance?

Business mileage is basically a blanket term for the expenses reimbursed by an employer for travel expenses of the employee for purpose of business travel. For sole traders, it shall cover the cost of buying and maintaining a vehicle for business purpose. Read more about business mileage allowance in our article. These can be claimed by a sole trader or reimbursed to employees, as the case may be, at actual cost or approved mileage rates.

These can be claimed by a sole trader or reimbursed to employees, as the case may be, at actual cost or approved mileage rates.

-

What is a Tax Code?

Tax code is an alphanumeric code used to work out how much income tax needs to be collected from a person's income.These codes generally start with a number and end with an alphabet, for eg. 1250L. The number in a tax code is the amount of tax-free income the person gets in that particular year. The letter in the tax code refers to personal circumstances which may affect their Personal Allowance.

-

How does Employment and support allowance aid people with disabilities or health conditions?

Employment and Support Allowance (ESA) is an allowance to help people with disability or health condition that affects how much you can work. Under ESA the government provides the applicants with either help in form of money to help with living costs in case they are unable to work or support to get back into work they can work. The applicant may be employed, self-employed or unemployed.

-

Is Jobseeker's Allowance (JSA) an unemployment benefit provided by the UK government?

Jobseeker's Allowance (JSA) is an unemployment benefit the UK government provides to people who are unemployed and actively seeking work. This allowance is provided to cover living expenses while the claimant is out of work. Payments of JSA Payments are usually made every 2 weeks. There are 3 types of Jobseeker’s Allowance (JSA):

- New style’ JSA

- Contribution-based JSA

- Income-based JSA

Application for contribution-based and income-based JSA can be made only if the applicant either:

- gets the severe disability premium, or is entitled to it; or

- got or was entitled to the severe disability premium within the last month and is still eligible for it.

-

What is Child Tax Credit?

Child tax credit is a benefit that a parent or carer gets if they are responsible for at least one child. This basically tops up the income of the one responsible for taking care of a child. It has been replaced by Universal Credit for most people. New claims for Child Tax Credit can be made if you:

- get the severe disability premium, or are entitled to it

- got or were entitled to the severe disability premium in the last month, and you're still eligible for it.

It can be claimed until the September following your child's 16th birthday or if they are in approved education or training, you can claim until their 20th birthday. The amount of tax credit you receive depends on the number of children you have, and if your child has any disabilities and whether you are making a new claim for Child Tax Credit or already claiming Child Tax Credit.

-

What is Working Tax Credit?

Working Tax Credit is a payment made by the government to people with low incomes in order to help them with day to day expenses. Whether a person id eligible for this credit depends on the hours of paid work they do each week and their income and circumstances. It has been replaced by Universal Credit for most people. A new claim for Working Tax Credit can be made if the claimant:

- gets the severe disability premium, or is entitled to it

- got or was entitled to the severe disability premium in the last month, and is still eligible for it

-

What is Rural Rate Relief Scheme?

Under rural rate relief, a business is not required to pay business rates if it is located in a rural area with a population below 3,000 and is either:

- the only village shop or post office, with a rateable value of up to £8,500

- the only public house or petrol station, with a rateable value of up to £12,500

You click here to contact your local council and check you're eligible and to apply for rural rate relief. You can to contact your local council and check you're eligible and to apply for rural rate relief.

-

When is a name considered 'same as' an existing name?

A name shall be considered 'same as' if the only difference with an existing name is either a punctuation mark, special character, word or character used commonly in UK company names or word or character that's similar in appearance or meaning to another from the existing name.

-

When is a name considered 'too like' an existing name?

A name shall be considered 'too like' if someone complains and Companies House agrees it's 'too like' a name registered before yours.

-

What is the difference between LLP and a limited partnership?

S. No. Basis Limited Liability Partnership (LLP) Limited Partnership (LP) 1 Law It is governed by Limited Liability Partnerships Act 2000. It is governed by Limited Partnerships Act 1907. 2 Partnership agreement There needs to be a formal LLP agreement place. No such requirement. 3 Partners There are two types of partners designated and ordinary. There are two types of partners limited and general. 4 Liability towards business debts The liability of ALL the partners is limited The liability of general partners is unlimited but of limited partners it is limited. 5 Management and control All partners can work in day to day management and control of the partnership business depending upon their roles and responsibilities defined in the LLP agreement. Limited partners have no say in the day to day management and control of the partnership business. Only general partners have the power to do so. 6 Mode of registration The LLP can be registered using the physical form, third party software or through formation agents. The partnership can be registered through physical form only. 7 Incorporation document An incorporation document needs to be submitted to Registrar for the incorporation of LLP No such requirement. -

What is Auto-enrolment Pension Reference Number?

A pension number is a unique number that's used to identify your pension and can usually be found at the top of your pension paperwork. If you can't find your pension number in your records, you should contact your pension provider for assistance. For the National Employment Savings Trust (NEST), this is known as the unique employer NEST ID.

-

Self Assessment

-

What is personal UTR (Unique Taxpayer Reference)?

Personal UTR (Unique Taxpayer Reference) is a 10 digit code. It is completely unique to each and every UK taxpayer who is a natural person. Whether the taxpayer is sole trader or an individual earning any income or part of a partnership, a personal UTR number is needed to file a Self-Assessment tax return online or via post. HMRC uses it to identify you for everything relating to your taxes.

-

Do I need to file a Self-assessment tax return SA100?

The constraints to file self-assessment tax return SA100 are:

- A person self-employed as a 'sole trader' and earning more than £1,000

- A partner in a business partnership

- A person may file a self-assessment return to claim some income tax reliefs

- A person may file a self-assessment return to prove he/she is self-employed, for example, to claim Tax-Free Childcare or Maternity Allowance

- A person whose, only income is from wages or pension but also has any other untaxed income, such as money from renting out a property, tips, and commission, income from savings, investments, and dividends, foreign income, etc.

- Most employees paying tax under the PAYE system are not required to file a tax return. However, some employees may have income that has not been taxed at source and needs to be declared to HMRC. Such a person shall do so by submitting a self-assessment tax return.

-

Who needs to file a personal tax return SA100?

The following persons need to file self-assessment tax return SA100:

- A person self-employed as a 'sole trader' and earning more than £1,000

- A partner in a business partnership

- A person may file a self-assessment return to claim some income tax reliefs

- A person may file a self-assessment return to prove he/she is self-employed, for example to claim Tax-Free Childcare or Maternity Allowance

- A person who's only income is from wages or pension but also has any other untaxed income, such as money from renting out a property, tips and commission, income from savings, investments and dividends, foreign income etc.

- Most employees paying tax under the PAYE system are not required to file a tax return. However, some employees may have income that has not been taxed at source and needs to be declared to HMRC. Such a person shall do so by submitting a self-assessment tax return.

To know more about self-assessment tax return filing due dates click here.You can also read our article on self assessment to know more about it.

-

When am I supposed to file the personal tax return?

The tax year for a personal tax return is 6 April current year to 5 April of next year.

The deadlines for filing personal tax returns (for the tax year 2020-21) are:

Paper tax return Midnight 31 October 2021 Online tax return Midnight 31 January 2022 Pay the tax you owe Midnight 31 January 2022 -

How do I make the advance payments by ‘Payments on Account’?

'Payments on account' mean advance payments made for your Self-Assessment tax bill. HMRC assumes that you will continue to earn at the same rate as the previous year, therefore, you will pay approximately the same amount of tax in the following year. Each year two payments on account must be made. Each payment is half the previous year’s tax bill. Each payment is due by midnight on 31 January and 31 July. To know more click here.

-

I am a sole trader, so for how long do, I need to keep my tax records?

You must keep your records for at least 22 months after the end of the tax year the tax return is for. HM Revenue and Customs (HMRC) may check your records to make sure you're paying the right amount of tax.

-

Can I claim for simplified expenses? How?

Claiming expenses on an actual basis requires the businesses to maintain records pertaining to those expenses. Simplified expenses can relieve your businesses from the burden of maintaining records. Your business expenses are calculated using flat rates and the resultant figure is claimed as business expense out of the net profits for the year. Once you have claimed simplified expenses you can no more claim actual expenses for the same. Simplified expenses can be claimed by sole traders and business partnerships that have no companies as partners. You can read more about simplified expenses in our article here.

-

Who can claim simplified expenses?

Simplified expenses can be used by:

- sole traders

- business partnerships that have no companies as partners

-

What kind of expenses can be claimed as simplified expense?

Flat rates for simplified expenses can be claimed for:

- business costs for vehicles

- working from home

- using business premises for personal use

All other expenses are claimed by working out the actual costs.

-

How should I register as a sole trader?

If you've never registered for self-assessment with HMRC ever before, then you need to register for it online on gov.uk website. Once you register, HMRC will set up your self-assessment online service account and send you a letter with your UTR.

You need to re-register online via form CWF1 if you've sent a self-assessment return online before. For this you'll need your 10 digit UTR (Unique Taxpayer Reference). To know where you can find your UTR click here.

Once you register, you will get a letter from HMRC within 10 business days (21 days if you're abroad) that will have an activation code for your online account which you will need while signing in to your online account for the first time.

-

Can I make changes in my self-assessment tax return after it is filed?

Yes, you can make changes to your self-assessment return either online or by post within 12 months from the filing deadline for the self-assessment return for the said period.

-

What are the Income Tax rates in UK?

The income tax rates in UK for current tax year i.e. from 6 April 2019 to 5 April 2020 are as follows:

Band Taxable income Tax rate Personal Allowance Up to £12,500 0% Basic rate £12,501 to £50,000 20% Higher rate £50,001 to £150,000 40% Additional rate over £150,000 45% -

What is self-assessment tax return filing due date?

The due date for filing self assessment tax returns are:

Paper tax return Midnight 31 October 2021 Online tax return Midnight 31 January 2022 -

What is the self-assessment tax payment due date?

The due date for paying self-assessment tax returns for the tax year 2020-21 is Midnight 31 January 2022.

-

How long do I need to keep accounting records as a sole trader?

You must keep your accounting records for a period of at least 5 years after the 31st January submission deadline of the relevant tax year.

-

Why do I file self-assessment (SA100) tax return?

Most people in the UK pay all their tax ‘at source’, for example, through Pay As You Earn (PAYE) if they are employed, and are not required to file a tax return. Self-Assessment therefore does not affect everyone and you will normally only need to complete a form if one or more of the following apply to you:

- You are working for yourself – you are self-employed;

- You are a partner in a partnership business

- You are a trustee or the executor of an estate.

The idea of Self-assessment is that you are responsible for completing a tax return each year if you need to, and for paying any tax due for that tax year. It is your responsibility to tell HM Revenue & Customs (HMRC) if you think you need to complete a tax return.

If you complete a Self-assessment tax return, you include all your taxable income, and any capital gains. You also claim any tax allowances or reliefs that you are entitled to on the tax return

SA100 is the form for carrying out a self-assessment of your (an individual’s) income and informing the HMRC. It is accompanied by several supplementary forms to detail out income from other sources like UK property, foreign income, etc. SA 100 along with relevant supplementary forms is called self-assessment return. You can read our article on ‘SA 100-things every taxpayer should know’ here.

-

How do I know the difference between advisory fuel rates (AFR) and approved mileage allowance (AMA)?

Firstly, advisory fuel rates (AFR) are used when the company’s car is used by you (employee) whereas approved mileage allowance (AMR) is used when your (employee’s) own car is used for business travel. Secondly and most importantly, AFR only covers fuel expenses since the employer is already paying for the car. On the other hand, AMA covers the cost of insurance, repair, maintenance, etc. AFR can be used to figure out how much of the annual business mileage is spent on fuel, regardless of the fact whether the company’s or own vehicle is used.

-

What are emergency tax codes?

1257L W1 and 1257L M1 codes or just 1257L X code are temporary codes. HMRC applies an emergency tax code if it doesn't have enough details about the amount of tax the person needs to pay. M1 is used when the pay is monthly while W1 is used when the pay is weekly. 1257L X can apply to either of these. M1/W1 or X code indicates that the tax shall be non-cumulative. In other words, the tax will be calculated based on the only current period's pay and not on the basis of year to date earnings.

A “cumulative” code (like 1257L) calculates tax due by taking into consideration rebate on any overpaid tax or recovery on any underpaid tax automatically. Suppose, if a person is not paid in a particular pay period a cumulative code would automatically give him/her benefit of the tax allowances for the no income period on the next payment but a non-cumulative code would not. In cases where HMRC does not issue a cumulative tax code before the end of the tax year, any overpayment gets rebated when the year is reconciled or when the person completes his/her self-assessment return. One always starts a new tax year with a cumulative tax code.

-

What is property allowance?

Property allowance is a tax exemption of up to £1,000 a year available only to individuals with income from land or property. This means that if the rental income is less than £1,000 then no tax is payable and also nothing needs to be informed to HMRC. But, if the rental income is more than £1000 then self-assessment tax return needs to be filed. One needs to choose between receiving the property allowance and deducting the actual expenses from rental income. Claiming actual expenses is advisable if this produces a rental loss, as no loss can be claimed if he/she elects to use the property allowance.

-

Who needs to make Payments on Account?

HMRC introduced a system called “payments on account” for assesses who pay most of their tax through Self-Assessment. If the Self-Assessment bill of a person is more than £1,000, then his/her tax needs to be paid on account. But, if more than 80% of one's income gets taxed through PAYE, then this system won't apply on him/her.

-

Am I eligible for a personal allowance?

- Everyone, including students, has something called a Personal Allowance. This is the amount of money you’re allowed to earn each tax year before you start paying Income Tax.

- For the 2021/22 tax year, the Personal Allowance is £12,570. If you earn less than this, you usually won’t have to pay any income tax.

- If your Income is above £1,00,000, basic personal allowance is reduced by £1 for each £2 you earn over the £1,00,000, limit.

- This means that if you earn £1,25,000 or more in 2021-22, you will receive no personal allowance and all your income is taxed.

-

Can I switch from claiming simplified expenses to claiming actual expenses?

Once your business opts for claiming simplified expenses it needs to stick to it throughout the life of the business or the life of asset regarding which simplified expenses are claimed.

-

Corporation Tax

-

For what purpose, the HMRC needs the company UTR (Unique Taxpayer Reference)?

The main purpose of a UTR number is to help HMRC identify tax payers. You will need your UTR number when completing and filing of corporation tax return and when someone is helping you with tax related matter.

Here is a sample letter containing the company UTR.

-

Is CRN (Company Registration Number) different from company UTR (Unique Taxpayer Reference)?

A Unique Taxpayer Reference is issued and used by HMRC to identify a particular company or organisation for tax purposes only. It consists of 10 digits.

A Company Registration Number (CRN) is immediately created and assigned by Companies House when a new limited company or LLP is incorporated. It is a unique 8-digit number or 6 numbers prefixed by 2 letters.

-

What is CT603?

CT 603 is a notice HMRC issues to a company to request the filing of a company tax return for corporation tax, including supplementary pages. If HMRC has sent company a 'Notice to deliver a Company Tax Return' (form CT 603), then the company must, by law, deliver a Company Tax return (CT 600). The said Company Tax return shall be prepared for the company's accounting period that is the same as or ends in the period specified in form CT603.

-

What is franked Investment Income?

Income in form of dividends paid to a company from earnings on which corporation tax has already been paid by the originating company is called franked investment income.

CT 603 is a notice HMRC issues to a company to request the filing of a company tax return for corporation tax, including supplementary pages. If HMRC has sent company a ‘Notice to deliver a Company Tax Return’ (form CT 603), then the company must, by law, deliver a Company Tax return (CT 600). The said Company Tax return shall be prepared for the company’s accounting period that is the same as or ends in the period specified in form CT603.

-

What is restitution interest?

If your company has made common law claims concerning tax paid ‘under a mistake of law’. If a restitution award is made, whether because of judgment or an agreement, THE INTEREST element of the award will be chargeable to corporation tax at a special rate of 45% instead of the normal rate (i.e., currently 19%). This interest is defined as restitution interest. It does not apply to any element of the award that represents the repayment of overpaid tax.

-

Why do I need the CT activation code?

A CT activation code is a 12-digit code that is needed to activate your company’s corporation tax account. Once you successfully enrol for the corporation tax online service, you will receive a letter containing the activation code within 7 days of enrolment. The activation code is valid for only 28 days from the date mentioned in the letter and you need to use it before that. If it expires then you will have to request a new activation code online. This can be done by signing in for HMRC online services and enrolling for the services again. But if the code is lost within 28 days, then sign in for HMRC online services and ask for a new code.

-

What is meant by surrenderable loss while claiming R&D tax relief?

As per section 1055 of Corporation Tax Act 2009 the company has a surrenderable loss if in an accounting period the company:

- obtains an additional deduction under section 1044 of the Corporation Tax Act 2009 in calculating the profits of a trade and it makes a trading loss in that period in the trade, or

- is treated as making a trading loss under section 1045 of the Corporation Tax Act 2009.

For expenditure incurred on or after 1 April 2015 the amount of the surrenderable loss shall be calculated as the lesser of:

- the amount of the unrelieved trading loss sustained in that period; and

- 230% of the related qualifying R&D expenditure.

Click here to read about R&D tax relief

-

What is meant by Unrelieved trading loss, while calculating surrenderable loss?

As per section 1056 of Corporation Tax Act 2009 the amount of the unrelieved trading loss is the amount of the trading loss less the sum of following:

- any relief that was, or could be obtained by making a claim to set the loss against profits of the same accounting period under section 393A(1)(a) of Income and Corporation Tax Act 1988,

- any other relief obtained in respect of the loss,

- any amount surrendered to group or consortium members.

Knowing unrelieved trading loss is used to calculate amount of surrenderable loss

-

When do I file the corporation tax return?

You need to file your company’s tax return within 12 months from the end of an accounting period to which it relates.

-

When do I pay my corporation tax?

The corporation tax bill needs to be paid by you within 9 months and 1 day from the end of an accounting period to which it relates.

-

What is meant by iXBRL tagging?

The Extensible Business Reporting Language (XBRL) is a standard used for tagging business data for computers. It involves applications of computer-readable tags to business data such that data is automatically processed by the software.

-

Why do I file the CT600 form?

Some organisations, such as limited companies, pay Corporation Tax on the profits that they make from trading and investment income. It’s also applicable to other organisations, like societies, associations, clubs and charities. They will have to submit a CT600, along with supporting documents, so that HMRC know how much Corporation Tax is due.

-

What is a company tax return?

A Company Tax Return is the financial information that most companies file with HMRC each year to report on their earnings, losses, loans and any other factors relevant to their tax liability. Companies use this information to calculate the Corporation Tax that they owe.

-

Can I make changes to my corporation tax return?

Yes, you can make changes to your corporation tax return either online or by post within 12 months from the filing deadline for the corporation tax return for the said period.

-

What is corporation tax rate?

Currently, corporation tax rate is 19%.

-

Can changes be made to corporation tax return after it is filed?

Yes, you can make changes to the corporation tax return of your company upto 12 months after the tax return filing deadline. This can be done either online or by sending a paper return to HMRC. Suppose you need to make changes in the return for the year ending on 30th November 2017, then deadline for filing the return will be 30th November 2018. Thus amenedments, if any, need to be made upto 30th November 2019.

-

What is Company Registration Number (CRN)?

A company number is officially known as a Company Registration Number (CRN). It is issued by Companies House immediately upon incorporation of a company. It is unique to a company and is displayed on the certificate of incorporation. A company must provide this number whenever it contacts Companies House.

It is important to note that company's CRN (company registration number) is not the same as company Unique Taxpayer Reference (UTR). Click here to know the difference between both of them.

-

What is the difference between dormant company for Companies house and Dormant company for corporation tax purposes?

A company is called dormant for Companies House if it had no 'significant transaction' in a financial year. If a company pays filing fees to Companies house, penalties for late filing of accounts and/or money paid for shares when the company was incorporated; then such transactions shall not amount to significant transactions and so the company shall still continue to be a dormant company.

A company shall be considered to be dormant for corporation tax purposes, if:

- It has stopped trading and has no other income like investment income, rental income etc.

- It is a new limited company that hasn't started its business.

- It's a flat management company.

- It is an unincorporated association or club owing less than £100 corporation tax.

-

IR35

-

How can I tell if I am an off-payroll worker or not?

A worker is involved in off-payroll working when they work for a client through their intermediary, often a personal service company (PSC), but would be an employee if they were providing their services directly instead of involving the arrangement of providing service through a PSC. An intermediary will usually be the worker’s personal service company. It could also be a partnership, a managed service company, or an individual.

-

Am I inside IR 35 Rules or outside?

Inside IR 35: The entity inside IR 35 you are required to pay tax & National Insurance Contributions on the entirety of your deemed salary, just like a permanent employee would have.

Outside IR 35: The entities outside IR 35 are deemed to be legitimate companies and they continue to operate and pay tax accordingly (as any other limited company would have).

-

Do IR 35 off-payroll working rules apply to my business entity?

Following persons shall be covered under IR 35 off-payroll working rules 2020:

- Public sector entities

- Private sector companies that satisfy at least two of the following conditions:

- Annual turnover of more than £10.2 million

- Balance sheet total more than £5.1 million

- More than 50 employees

Any person is other than the company, LLP, an unregistered company, an overseas company with an annual turnover of more than £10.2 million.

If the parent of a group is medium or large, their subsidiaries will also have to apply the off-payroll working rules.

-

Which parties are affected by IR35 off-payroll working rules?

There are 5 parties involved in the labour supply chain:

- Worker

- Intermediary - Workers own personal service company (PSC)

- Fee payer (maybe)

- Agencies (maybe)

- Client - for whom work is being done

'Clients' covered under IR35 wef April 2020 are:

- Every public company

- Every private company which satisfies 2 or more of the following

conditions:

- Annual Turnover of more than £10.2 million

- Balance sheet total of more than £5.1 million

- 50 or more employees

- Every entity, other than company, limited liability partnership, unregistered company and overseas company with an annual turnover of more than £10.2 million.

- If the parent of a group is medium or large, their subsidiaries will also have to apply the off-payroll working rules.

-

What is IR35?

IR35 or off payroll working rules refer to an anti-avoidance tax legislation designed to collect tax and National Insurance at a rate similar to employment, where the contractor is an employee in all but name.

Click here to read about IR 35 in detail.

-

What is CEST?

Check Employment Status for Tax service (CEST) is a tool that has been developed by HMRC to help the user in determining the employment status of a person, i.e., whether the said person is employed or self-employed for tax purpose. It is pertinent to note here that the tool assumes there is a contract in place between employer and employee to see whether the engagement can be classed as employment or self-employment. HMRC claims it to provide accurate results and that it shall stand by the result produced by the tool provided the information input is accurate and the tool is used in accordance with the guidance.

-

What is a Managed Service Company (MSC)?

A Managed Service Company (MSC) has a separate set of owners and organisers managing a group of contractors. Management Service Company differs from Personal Service Company. MSC manages and controls the affairs of the business, not the contractor. Further, MSC are subject to different regulations by HMRC.

-

What is a Personal Service Company (PSC)?

A Personal Service Company is a limited company set up to provide services of a single contractor. In other words it is generally an “intermediary” taking the form of a limited company. This company is generally owned 100% by the contractor, and he/she is usually the sole director too.

Forming a PSC has many benefits. Firstly, the liability of the sole contractor becomes limited. Secondly, it provides a more formal and professional way to present services to their clients. Also, company form of business structure enables managing taxes efficiently.

-

VAT

-

Can I reclaim VAT paid on purchases made before registering into VAT?

You can reclaim VAT on the following purchases and services made before registering into VAT:

- 4 years for goods you still have or that were used to make other goods you still have.

- 6 months for service.

It is worth noting that you can only reclaim VAT on supplies for the business which is now registered for VAT. Also, these supplies must be used for ‘business purposes’ only.

Click here to read more about claiming back VAT.

-

How can VAT flat rate scheme aid me?

Using the Flat Rate Scheme you pay VAT as a fixed percentage of your VAT inclusive turnover. The actual percentage you use depends on your type of business.

A first year discount. If you are in your first year of VAT registration you get a one per cent reduction in your flat rate percentage until the day before the first anniversary you became VAT registered.

VAT Flat Rate Scheme might not be right for your business if:

- you buy mostly standard-rated items, as you cannot generally reclaim any VAT on your purchases

- you regularly receive a VAT repayment under standard VAT accounting

- You making a lot of zero-rated or exempt sales.

-

How does the VAT accounting period work?

You usually submit a VAT return to HMRC every 3 months. This period of time is known as your ‘accounting period. However, your VAT accounting period will comprise of 12 months in case you have opted for VAT Annual Accounting Scheme.

-

When should I submit my VAT return?

The due date for submitting the vat return online is 1 month and 7 days after the end of a VAT accounting period.

-

What is the due date for paying the VAT bill?

The due date for submitting the return online and paying HMRC are usually the same - 1 month and 7 days after the end of a VAT accounting period.

-

What is the due date for submitting VAT return for businesses covered under annual accounting scheme?

If you opt for annual accounting scheme you need to file VAT return only once a year. Your VAT accounting period will comprise of 12 months. The VAT return shall be due in 2 months from the end of VAT accounting period.

-

What is the due date for paying VAT bill for businesses covered under annual accounting scheme?

If you're covered under the annual accounting scheme you need to make advance payments towards your VAT bill during a VAT accounting period and a final payment once you file your VAT return. HMRC will tell you in writing when your installments are due and how much they'll be.

PAYMENT PAYMENT DEADLINE IF ANNUAL ACCOUNTING SCHEME IS USED Monthly Due at the end of months 4, 5, 6, 7, 8, 9, 10, 11 and 12 Quarterly Due at the end of months 4, 7 and 10 Final payment Within 2 months from month 12 If the due date falls on a weekend or bank holiday, your payment must clear HMRC's bank account on the last working day before it, unless you pay by Faster Payments.

-

What is input tax credit can I reclaim it?

You can usually reclaim the VAT paid on goods and services purchased for use in your business.

You may be able to reclaim VAT paid on goods or services bought before you registered for VAT if the purchases were made within certain time limits.

-

If my business is VAT registered do I need to charge output VAT?

If a business is registered for VAT then it must charge VAT on all its taxable sales. There's no option to decide not to charge VAT to certain customers.

-

What is VAT?

Value added tax, or VAT, is the tax you have to pay when you buy goods or services.

Businesses with a turnover of more than £85,000 must register to pay and charge VAT on the products and services they buy and sell. Other businesses can choose to register for VAT voluntarily.

Click here to read the detailed article on understanding Value Added Tax.

-

Can I claim VAT credit if I sell zero-rated supplies?

When goods or services are zero rated they are still called VAT able supplies. The VAT rate on such goods and services is zero. Hence, a supplier supplying goods at zero rated can reclaim credit on purchases.

-

All my sales are zero rated. Do I still need to register for VAT?

When goods or services are zero-rated, they are still called VAT able supplies. The VAT rate on such goods and services is zero. So, if the taxable turnover goes above £85,000 the supplier needs to register under VAT.

-

What are the VAT rates in the UK?

There are three VAT rates prescribed:

- Standard rate is charged on most of the goods that are 20%,

- Reduced rate is charged on domestic fuel power, mobility aids, etc. that is 5%

- Zero-rate - the goods and services covered under this rate are VAT taxable and charged to customers at 0%. Though practically no VAT is collected but the businesses are still required to record such sales in their VAT account and report them in VAT return. Zero rates are applicable on books, newspapers, motor cycle helmets, children’s clothes and shoes etc.

- These are the 3 rates that are prescribed in the UK.

Exempt supplies- Some goods and services are exempt from VAT. No VAT is charged on exempt goods.

-

How can partly exempt businesses claim an input tax credit on capital goods?

The partly exempt business can claim tax credit on capital goods through capital goods scheme. Under this scheme VAT recovery is adjusted based on the taxable use. As the taxable use increases, a further amount of input tax can be claimed and, as it decreases, equivalent input tax already claimed needs to be repaid. Click here to know more about capital goods scheme.

-

Do Vat reverse charges apply to EU transactions only?

No. VAT is generally recorded, collected, and paid by the seller. But if a transaction is covered under reverse then the VAT will be recorded by the buyer instead of the seller. In such situations, VAT is paid by the buyer directly to HMRC instead of the seller.

However, the VAT reverse charge applies to intra-community EU transactions, and with effect from 1st October 2020, this will also apply to industry services.

-

What is MTD for VAT?

MTD refers to Making Tax Digital. With effect from1st April 2019, all the VAT registered businesses with an annual turnover of more than £85,000 were mandated to maintain their VAT records digitally and file the VAT returns through MTD-compatible software. Businesses with a taxable turnover less than the VAT threshold can voluntarily opt for it. Click here to read more about Making Tax Digital.

-

What is the difference between zero rated supplies and exempt supplies in VAT?

Zero rated: The goods and services covered under this rate are VAT taxable and charged to customers at 0%. Though practically no VAT is collected but the businesses are still required to record such sales in their VAT account and report them in VAT return. Also, the best part is that a claim can be made for any INPUT VAT paid while producing/acquiring zero-rated goods. Zero rate is applicable on books, newspapers, motor cycle helmets, children's clothes and shoes etc.

Exempt supplies: No VAT is charged on goods that are exempt, and such turnover is neither required to be reported in a VAT return nor can you claim back the INPUT VAT charged on your inputs. Exempted supplies include sponsored charitable events, Admission charges by charities, Charitable fundraising events etc. If a business only supplies VAT exempt goods, then such business is neither required nor allowed to register for VAT.

-

What is a VAT group?

A group of companies connected to each other may choose to file a single VAT return. Such group of companies are treated as single entity and so are called a VAT group.

Making VAT group facilitates two or more eligible persons to account for VAT under a single registration number and allows any one of the eligible persons within the group acting as the representative member.

-

What is VAT return?

VAT return is basically a form that depicts the amount of VAT owed to HMRC or the amount they owe to you. It shows total sales and purchases, amount of VAT owed, amount of VAT reclaim, VAT refund from HMRC for a particular VAT accounting period.

-

Can I correct my VAT return?

Providing the errors meet certain conditions, you do not need to tell HMRC about them – you can simply correct them by adjusting your next VAT return.

You can adjust your current VAT return to correct errors on past returns as long as the errors:

- are below the reporting threshold;

- are not deliberate; and

- Relate to an accounting period that ended less than four years ago. Or you can send form VAT652 to the VAT Error Correction Team.

-

What are the different VAT flat rates?

The different VAT flat rate schemes are as follows:

- Limited Cost Business: A business that spends a small amount on goods is classed as a ‘limited cost business’ if goods cost less than either:

- 2% of your turnover,

- £1,000 a year (if your costs are more than 2%)

- If a business satisfies the condition of limited cost business then it has to pay a higher rate of 16.5%.

- Others: If the business isn’t a limited cost business, the VAT flat rate will depend on the type of business. Click here to know the flat rates applicable on different types of business.

- Limited Cost Business: A business that spends a small amount on goods is classed as a ‘limited cost business’ if goods cost less than either:

-

What is the VAT Number?

A VAT-registered number is a unique identification issued to businesses that are registered to pay VAT. Businesses can find their VAT number on their VAT registration certificate issued by HMRC.

A UK VAT number is nine (9) digits long, with two letters at the front indicating the country code of the registered business. For example, for Great Britain (UK), the first two digits of the VAT code are GB.

If you’re dealing with a supplier in another EU country then its VAT number will follow a different format, with its own unique country code. HMRC provides a list of ID formats from European Union member states on their website.

-

Is it important to maintain VAT digitally and file returns through MTD?

From April 2019, VAT registered businesses and organisations with taxable turnover above the VAT threshold of £85,000 are required to:

- Maintain accounting records digitally in a software product or spread sheet. As a result, maintaining paper records has ceased to meet the legal requirements in tax legislation.

- Submit VAT returns to HMRC using a compatible software product that can access HMRC’s API (Application Program Interfaces) platform.

-

PAYE

-

What are the various PAYE forms?

There are several PAYE forms in use. Each has its own purpose.

Form P60- A P60 form is that explains how much you have earned over the tax year (06 April 2021 to 05 April 2022). It is also includes how much you have paid in national insurance contributions and PAYE tax.

Form P45- When you leave a job, your former employer should issue with a P45 form this is included your salaries, national insurance contributions, PAYE tax up to leaving date. You will need your P45 when changing the jobs, as your new employer will use it to make sure you are put in correct tax code.

Form P11D- A P11D form is sent to HMRC by UK employers outlining the cash value of any work-related taxable expenses and taxable benefits you've received over the tax year (6 April-5 April). These are only benefits or expenses that have not already been included in your wages.

There are currently 14 sections on the P11D:

- Section A – Assets Transferred

- Section B – Payments made on behalf of the employee

- Section C – Credit Cards and vouchers

- Section D – Living Accommodation

- Section E – Mileage Allowances

- Section F – Cars and car fuel

- Section G – Company Vans

- Section H – Beneficial Loans

- Section I – Medical Health

- Section J – Qualifying Relocation Payments

- Section K – Services Supplied

- Section L – Assets placed at employee’s disposal

- Section M – Other Items

- Section N – Expenses Payments

-

From where can I locate the PAYE payment reference number?

You can find on any correspondence you receive from HMRC, like tax forms, payslips, P45 and P60 forms. It is also in the welcome pack you receive when you first register your business.

-

What is the accounts office reference number for PAYE?

Your Accounts Office Reference Number is a unique, 13 character code which will be shown on the letter you received from HMRC when you first registered as an employer.

You will be required to put in your Accounts Home Office Reference Number when you intend to make PAYE payments to the HMRC.

-

Can I payroll the 'benefits in kind'?

Yes, benefits in kind can be payrolled if the employer has registered with HMRC for using the 'payrolling employee's taxable benefits and expenses service'. All the benefits can be payrolled except employer providing accommodation and interest free and low interest loans. These needs to be reported in P11D even if you’re payrolling other benefits for the same employees. Further, if company car benefits are payrolled then there is no need of P46.

If the employer intends to payroll benefits and expenses then he/she needs to register for payroll before the start of tax year in which he/she wishes to begin running it.

-

Do I require P11D even if the benefits are payrolled?

If benefits in kind are payrolled then there is no requirement of submitting P11D form. However, all the benefits except employer providing accommodation, interest free and low interest loans can be payrolled. Hence, these need to be reported in P11D even if you’re payrolling other benefits for the same employees.

Further, you need to complete and file form P11D(b) to report Class 1A National Insurance contributions on benefits in kind despite payrolling them.

-

What is P87 form?

P87 is a form that can be used by employees to claim tax relief for allowable employment expenses. If the allowable expenses are less than £2,500, the employee can claim tax relief through P87 form, but if the allowable expenses are more than £2,500 then these can be claimed only by filing a self-assessment return.

-

If benefits in kind are payrolled, then is there any requirement to file P11D?

If benefits in kind are payrolled then prima facie there is no requirement of submitting P11D form.

However, all the benefits except employer providing accommodation, interest free and low interest loans can be payrolled. Hence, these need to be reported in P11D even if you're payrolling other benefits for the same employees.

Further, you need to complete and file form P11D(b) to report Class 1A National Insurance contributions on benefits in kind despite payrolling them.

-

What records must be maintained for the requirements for PAYE?

You must collect and keep records of:

- What you pay your employees and the deductions you make.

- Reports you make to HM Revenue and Customs (HMRC).

- Payments you make to HMRC.

- Employee leave and sickness absences.

- Tax code notices.

- Taxable expenses or benefits.

- Payroll Giving Scheme documents, including the agency contract and employee authorisation forms

-

For how long do I need to keep the accounts according to HMRC?

The records must be maintained for 3 years from the end of the tax year they relate to. HMRC may check your records to make sure that the employer is paying the right amount of tax. Click here to read more about PAYE and payroll.

Click here to read more about PAYE and payroll.

-

What is Employer Payment Summary (EPS)?

EPS refers to Employer Payment Summary. It is basically used to claim refunds/recoverable amounts from HMRC or making declarations to HMRC. Few situations in which EPS needs to be filed are:

- For recovering statutory payments

- For reporting Apprenticeship levy

- For recovering Construction Industry Scheme (CIS) deductions suffered

- For informing HMRC that you have ceased using PAYE scheme, etc.

- For making an election to claim the employment allowance.

-

What is Full Payment Submission (FPS)?

FPS refers to Full Payment Submission. FPS is sent to HMRC to inform HMRC about the payments made to employees and the deductions made. It contains information like starter and leaver information, employee details, employee payment and deduction information etc.

-

When to send EPS?

Employer Summary Scheme (EPS) needs to be sent to HMRC by the 19th of the following tax month to apply any reduction (for example statutory pay) on what you'll owe from your FPS.

-

When to send FPS?

Full Payment Submission (FPS) needs to be sent to HMRC on or before each payday even if taxes and National Insurance are paid to HMRC quarterly or monthly.

-

What is payroll?

Payroll refers to the process of evaluating employee's pay, deducting income tax and national insurance contributions and reporting the same to HMRC.

-

What is PAYE?

PAYE refers to the system of Pay As you Earn. It is a system used by HMRC to collect Income tax and NI contributions from employee's pay as they earn it.

-

Can I choose to payroll some benefits and not all?

When you register to payroll benefits on the online service, you select the benefits you want to payroll. Therefore, you can choose which benefits in kind you wish to payroll and which you wish to process through form P11D. You may even choose to exclude employees who you will not payroll benefits for, i.e. for such employees you will continue submitting form P11D.

-

Do I need to register for payrolling benefits in kind every year?

Registering to payroll benefits in kind is a one off requirement. You do not need to register for it every year. Click here to registering to payrolling benefits online.

-

Is it compulsory to payroll benefits in kind?

No, it is not necessary to payroll benefits in kind nor does HMRC wishes to make it compulsory in future. You can instead report the benefits in kind through form P11D.

-

Will tips given count as benefit in kind?

Tips and gratuities paid to employees are not benefits in kind. Instead if the employer distributes the tips then it shall form part of salary and be subject to tax and NICs as usual.

-

Is there a deadline for filing form P11D?

Yes, P11Ds must be submitted to HMRC before 6 July 2022 for the tax year 2021-22. You’ll get a penalty of £100 per 50 employees for each month or part month your P11D(b) is late. You’ll also be charged penalties and interest if you’re late paying HMRC.

-

What is form P11D(b)?

A P11D form is sent to HMRC by UK employers outlining the cash value of any work-related taxable expenses and taxable benefits you've received over the tax year (6 April-5 April). These are only benefits or expenses that have not already been included in your wages.

-

Can I deregister from payrolling of benefits?

Yes, if you wish to deregsiter from payrolling of benefits you can do it before the start of tax year using the online service.

-

If I register for payrolling of benefits, can I choose to payroll benefits for some and not for others?

Yes, you can choose to exclude employees for whom you do not wish to payroll benefits in kind. For such employees you will continue submitting form P11D.

-

What is the PAYE Reference number?

The PAYE reference number is given to every business that registers with HMRC as an employer. It’s a unique set of letters and numbers used by HMRC and others to identify your firm.

This reference is made up of two parts: a three-digit HMRC office number and a reference number unique to your business. It will usually look something like 123/A45678 or 123/AB45678 (though there can be exceptions).

-

Export-Import

-

What are Transitional Simplified Procedures(TSP)?

In order to simplify the procedural requirements for movement of goods between the EU and the UK post Brexit, TSP have been introduced. TSP aim to make import of goods easier for an initial period of one year to give businesses time to prepare for usual customs procedures while importing from the EU. The businesses registered for TSP will be able to postpone payment of import duty until one month after imports. Further, they'll be required to give reduced information in the import declaration when the goods are crossing the border and give full declaration only after the goods have crossed the border.

-

What is meant by Common Transit Convention(CTC)?

Common Transit Convention (CTC) allows quicker movement of goods across the borders of common transit countries. The common transit countries are EU member states, Iceland, Norway, Liechtenstein, Switzerland, Turkey, North Macedonia, Serbia. The customs declaration and payment of customs duty needs to be paid only when the goods reach final destination. This facilitates cash flow benefits and reduces administrative burdens.

-

Compliance

-

Is it mandatory to report Person with Significant Control (PSC) to Companies House?

Yes, the companies need to mandatorily report Person with Significant Control (PSC) changes to Companies House as and when they happen. Besides reporting changes to Companies House, companies are also required to maintain a Register of People with Significant Control. If you fail to comply with these requirements you could be committing a criminal offence.

-

What are the compliance obligations of a dormant company?

- Filing of dormant accounts to Companies house- Dormant accounts should include a balance sheet and any relevant notes for the past financial year. The accounts will have to be filed with Companies House every year, no later than 9 months after the end of the company’s financial year.

- Filing of confirmation statement to Companies House- You also required to provide an annual confirmation statement for a dormant company every 12 months. The due date for filing a confirmation statement for the dormant company is 12 months from the date the company was incorporated and then needs to be filed every 12 months. It must be filed within 14 days from this date. It is to be filed even if there is no change to the relevant details.

Click here to know more about the compliances required by a dormant company.

-

What are the filing requirements for a dormant company?

- Filing of dormant accounts to Companies house- Dormant accounts should include a balance sheet and any relevant notes for the past financial year. The accounts will have to be filed with Companies House every year, no later than 9 months after the end of the company's financial year.

- Filing of confirmation statement to Companies House- You are also required to provide an annual confirmation statement for a dormant company every 12 months. The due date for filing a confirmation statement for the dormant company is 12 months from the date the company was incorporated and then needs to be filed every 12 months. It must be filed within 14 days from this date. It is to be filed even if there is no change to the relevant details.

Note: As long as the company is inactive throughout the financial year there won't be any tax liabilities and it won't have to file a tax return. However, in cases when company was previously trading you need to call HMRC on 0300 200 3410 or write a letter addressed at Corporation Tax Services, HM Revenue and Customs, BX9 1AX, United Kingdom to tell them that the company is dormant and that you shall thereby not submit any tax return.

Click here to know more about compliances required by a dormant company.

-

How do I inform the HMRC about dormancy?

You can inform HMRC about the dormant status by calling on 0300 200 3410 or you can update the same over the Web chat Or write a letter addressed at Corporation Tax Services, HM Revenue and Customs, BX9 1AX, United Kingdom.

-

Company

-

Can I be a Company Director?

Almost anyone can be a director of a UK limited company. There are very few barriers to appointment, which makes company formation an accessible option for many people. Whilst no specific qualifications are required, the role of company director does involve a great deal of responsibility, so there are certain restrictions as below:

- You must be over the age of 16.

- You must not have been disqualified from acting as a company director.

- You cannot currently be in bankruptcy (unless a court has given you permission to act for a particular company).

- You must not be subject to any UK government restrictions

- You must not have been restrained by a court from becoming a company director.

Also, as a director, you’re legally responsible for running the company and making sure information is sent to us on time.

- the confirmation statement

- the annual accounts, even if they’re dormant

- any change in your company’s officers or their personal details

- a change to your company’s registered office

- allotment of shares

- registration of charges (mortgage)

- any change in your company’s people with significant control (PSC) details

-

What are the compliance obligations of a Company Director?

A company does not have its own physical existence. The Board of Directors is basically the soul and body of the company. As a result anything required to be done by the company under the Companies Act, 2006 is to be carried out by the Directors unless otherwise provided (e.g. Passing resolutions required to be passed at a general meeting etc.). Most important obligations as required to be complied by a Company Director:

- Ensure that the company has filed accounts with Companies House and HMRC on or before due date.

- Make sure that the corporation tax returns are filed with HMRC on time.

- Filing confirmation statement to Companies House.

- Maintain various statutory registers like- register of charges, register of members, register of directors etc.).

-

What is Person with Significant Control (PSC)?

A Person with Significant Control (PSC) is an individual who meets any one or more of the following conditions in relation to a company:

- directly or indirectly holding more than 25% of the shares

- Directly or indirectly holding more than 25% of the voting rights

- Directly or indirectly holding the right to appoint or remove the majority of directors

- he/she has the right to exercise, or actually exercising, significant influence or control

- he/she has the right to exercise, or actually exercising, significant influence or control over the activities of a trust or firm which is not a legal entity, but would itself satisfy any of the first four conditions if it were an individual.

These need to be reported to various authorities. Click here to know more.

-

What is a Confirmation Statement?

In addition to financial statements, all Companies and LLPs are required to complete a Confirmation Statement. This is an annual statement filed by companies to Companies House in every 12 month review period to update any changes related to:

- Principal business activities or SIC codes,

- Statement of capital (paid/unpaid share capital or classes of shares),

- Shareholder information, and

- Trading status of shares and exemption from keeping a register of PSC.

-

Information to mention in a confirmation statement.

Companies House introduced the annual confirmation statement in June 2016. It’s designed to streamline the process of reporting information about your company.

An annual confirmation statement filing confirms the following information:

- Information about the company’s directors

- Information about the company’s secretary (if appointed)

- The company’s registered office address

- The company’s core business activities (SIC codes)

- Details of any shareholders

- Issue of shares

- Person(s) of significant control (PSC)

-

Do I need to file a confirmation statement for a dormant company?

Every company, including dormant and non-trading companies, must file a confirmation statement. It confirms the information Companies House hold about your company is up to date. You may simply click here to view the same on their official website.

The due date for filing a confirmation statement is 12 months from the date the company was incorporated or the date you filed your last confirmation statement. It must be filed within 14 days from this date. It is to be filed even if there is no change to the relevant details.

-

How can I make my dormant company active?

To make a previously dormant company active, inform HMRC within 3 months from the date company starts trading. It can be done by signing in to company’s HMRC gateway account and registering the company as active.

-

What is an umbrella company?

An umbrella company is a standard UK limited company. It acts as an ‘employer’ on behalf of its contractor employees. The recruitment agency shall enter into a contract with umbrella company, on behalf of the contractor who will be carrying out the work for the end client. Another contract, i.e. employment contract is to be signed between umbrella company and the contractor employee. Once the work is completed, the contractor employee shall submit a timesheet to both his recruitment agency, and umbrella, showing the number of hours he/she worked. The umbrella company will raise an invoice to the recruitment agency, which will subsequently bill the end-client. As soon as the umbrella company receives payment from the agency, they can prepare employee’s payroll and pay him/her a salary, allowing deductions for employment taxes, the pre-agreed umbrella fee/margin, personal taxes, and pension contributions (if applicable). They will also reimburse for certain allowable expenses he/she might have claimed – such as mileage.

The umbrella company is created as a special purpose entity to lessen the compliance burden. Instead of working as a contractor to the company yourself and getting stuck in hassles of compliances required to be done by a contractor, one could simply enter into employment contract with an umbrella company and work for the client. In this case the umbrella company shall carry out all the administrative activities like running your payroll, paying taxes and dealing with HMRC etc. Also, you could be able to claim work related expenses, holiday pays, workplace pension scheme etc. All you need to do is submit your time sheet and expenses and wait to get paid; the umbrella company will do all the paper work for you.

The umbrella company is created as a special purpose entity to lessen the compliance burden. Instead of working as a contractor to the company yourself and getting stuck in hassles of compliances required to be done by a contractor, one could simply enter into employment contract with an umbrella company and work for the client. In this case the umbrella company shall carry out all the administrative activities like running your payroll, paying taxes and dealing with HMRC etc. Also, you could be able to claim work related expenses, holiday pays, workplace pension scheme etc. All you need to do is submit your time sheet and expenses and wait to get paid; the umbrella company will do all the paper work for you.

From the client’s point of view, it needs not run payroll, provide any employment benefits etc. All these need to carry out by Umbrella Company only.

-

What is a Personal Service Company (PSC)?

A Personal Service Company is a limited company set up to provide services of a single contractor. In other words it is generally an “intermediary” taking the form of a limited company. This company is generally owned 100% by the contractor, and he/she is usually the sole director too.

Forming a PSC has many benefits. Firstly, the liability of the sole contractor becomes limited. Secondly, it provides a more formal and professional way to present services to their clients. Also, company form of business structure enables managing taxes efficiently.

-

What is a Managed Service Company (MSC)?

A Managed Service Company (MSC) has a separate set of owners and organisers managing a group of contractors. Management Service Company differs from Personal Service Company. MSC manages and controls the affairs of the business, not the contractor. Further, MSC are subject to different regulations by HMRC.

-

For how long does a company needs to keep its accounting records?

Company's accounting records need to be kept for 6 years from the end of the financial year they relate to, or longer if:

- they show a transaction that covers more than one of the company's accounting periods

- the company has bought something that it expects to last more than 6 years, like equipment or machinery

- Company Tax Return was sent late

- HMRC has started a compliance check into your Company Tax Return

-

How do I know my company falls under small company accounts?

Companies whose annual turnover must:

- not be more than £10.2 million,

- the balance sheet total must be not more than £5.1 million.

- The average number of employees must not be more than 50,

Only then your company can be qualified as a small company. To know how to do bookkeeping for these companies click here.

-

How do I know my company falls under micro company accounts?

Micro company is a company that fulfils any two of the following:

- Companies whose annual turnover of £632,000 or less,

- the balance sheet total is £316,000 or less,

- The average number of employees must not be more than 10.

-

Can I extend accounts filing deadline?

Yes, you can apply to extend your accounts filing deadline and before applying the extension you will require the information as listed below:

- The company number.

- An email address.

- Information about your extension reasons.

- any documents that support your application (optional)

-

Can my company change its accounting period?

Yes, you can extend or shorten the current accounting period by changing the current or the immediately previous accounting reference date. You need to inform Companies House for change of accounting reference date in form AA01. The submission should be done before the due date for filing the accounts of period that you wish to change. This change can be done using Companies House’s software filing or online filing services or by sending the relevant paper forms.

-

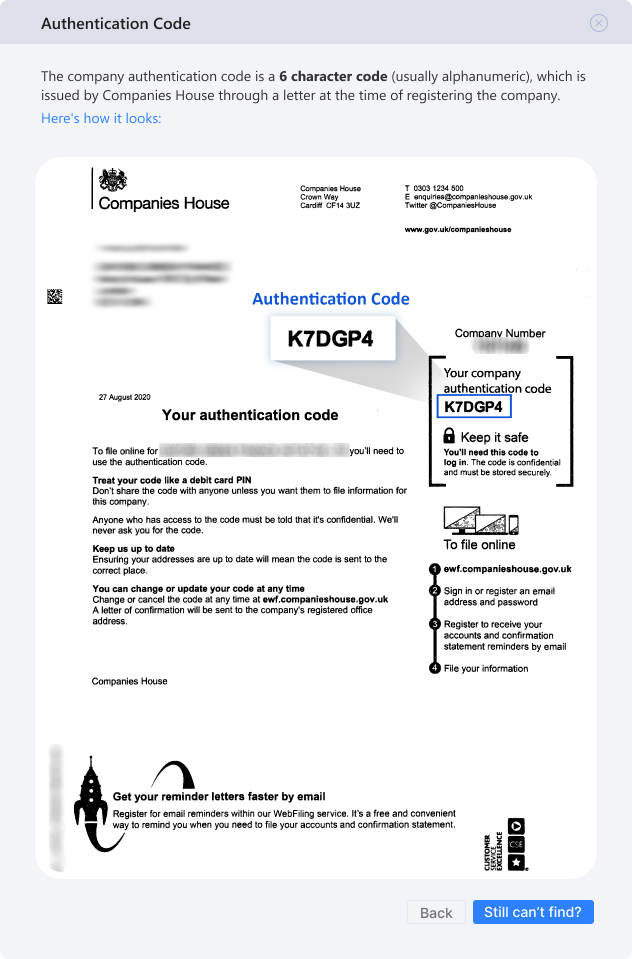

Why do I need a company authentication code?

The authentication code is a 6 digit alphanumeric code issued by us to each company. The authentication code provides access to the Companies House Web Filing service. This can be used to file various documents online. This enables a company to easily update the current appointments and file statutory documents.

-

How do I close a company?

To apply to strike off your limited company, you must send Companies House form DS01. This must be signed by a majority of the company’s directors. When your company is dissolved, all the remaining assets will pass to the Crown (including any bank balances).

-

What is the difference between dormant and a non-trading company?

A company which has not commenced trading since incorporation is called a dormant company. While a company which was previously trading but isn't active and trading anymore is termed as a non-trading company.

A non-trading company may be receiving other incomes like rent, interest and/or maybe paying expense like rent, bank charges etc. However, to maintain a dormant status, the company shall not be have any significant accounting transaction.

-

What is a 'close company'?

A close company is a company:

- which is under control of-

- five or fewer participators or

- any number of participators if those participators are directors,

- more than half the assets of which would be distributed to five or fewer participators, or to participators who are directors, in the event of the winding up of the company.

- which is under control of-

-

What is the due date for filing company accounts?

If you are filing your company's first accounts and those accounts cover a period of more than 12 months, you must deliver them to Companies House:

- within 21 months from the date of incorporation in case of private companies

- within 18 months from the date of incorporation in case of public companies

- 3 months from the accounting reference date whichever is longer

The time allowed for filing company’s first accounts for the subsequent years, to Companies House is:

- 9 months from the accounting reference date for a private company

- 6 months from the accounting reference date for a public company

When a company shortens its accounting period, the new filing due date will be the longer of the following two options;

- 9 months for a private company (or 6 months for a public company) from the new accounting reference date